ThePeachPit Model Portfolio Vol. VIII

ThePeachPit Model Portfolio Vol. VIII

This week was relatively slow on the research front. Decided to take the end of the week off to travel back home to Houston, Texas, to attend the Casa De Montecristo Texas Cigar Festival with my dad. I went a little out of my way at the festival and loaded up on some Perdomo 10th anniversary maduro cigars, some Plasencia Alma Fuertes, Camacho Ecuadors, and some EP Carrilo Blacks. Looking forward to enjoying a few premium cigars with the family before rounding back home!

Trading Ideas

As we approach the bitcoin halving event later this week, I felt compelled to tear into one of the big holders of the cryptocurrency, MicroStrategy. Though the firm will not directly be affected by the halving per se, the asset value has historically been well-received following the event.

I personally do not participate in crypto trading, not necessarily because I do not see value in the product, but because the price is so volatile, and I do not wish to give it my full attention. My mantra is that if you can achieve similar returns trading other assets, stick to what you know and don’t deviate from the program.

MicroStrategy (NASDAQ: MSTR) 4/11/2024

QuantumScape is a post-SPAC company that has remained in the development stages for solid-state lithium battery technology. The firm has yet to reach production stages, and as a result, has yet to generate any revenue. Though the firm recently released six prototype batteries to various OEMs, including Ford and Volkswagen, I expect the company is biting off more than they can chew in the wake of the slowing EV adoption in favor of hybrid vehicles. I also anticipate the firm to face an uphill battle in producing these batteries to scale at a profit as the automotive industry seeks to reduce the cost of producing their electric vehicles for the average consumers. With the battery being the most expensive cost of production, I anticipate these factors to significantly weigh in when the OEMs undergo their rigorous testing phase.

QuantumScape (NYSE: QS) 4/9/2024

Given the recent events in the Middle East, I’m curious to see how uranium stocks react. Equity futures on Sunday, 4/14/24, appeared positive going into the first trading day post-attack, which may suggest investors are shrugging it off as a nonissue. Though it is too soon to determine the full effect of any retaliatory action, I anticipate this skirmish to be properly addressed, whether directly from Israel or with assistance by the US.

UEC sold off into the end of the trading day on Friday, 4/12/24 after touching the top end of the price range. I expect this stock to remain relatively range-bound with respect to tactical trading given the heavy institutional involvement in the uranium sector.

DELL experienced a pretty big slide after reaching their high watermark at $136/share. The name has performed as expected going into the bull run and is going through a retracement period. Where the stock goes from here is up in the air. I anticipate the mid-$130s to act as a ceiling until we get more clarity on the company’s growth trajectory, whether it’s an intermittent update or the next quarterly earnings. I’m still running my corporate vs. consumer AI device thesis and anticipate this to weigh in on the server/PC market for the time being. HPE is expected to report a week prior to DELL at the end of May, so we could potentially gain some insights into the AI-enabled PC refresh cycle. INTC reports their next earnings on 4/25/24 and AMD reports at the first of May. These two firms may provide a stronger signal relating to the durability of the PC industry. I’ll update each of these firms as they report.

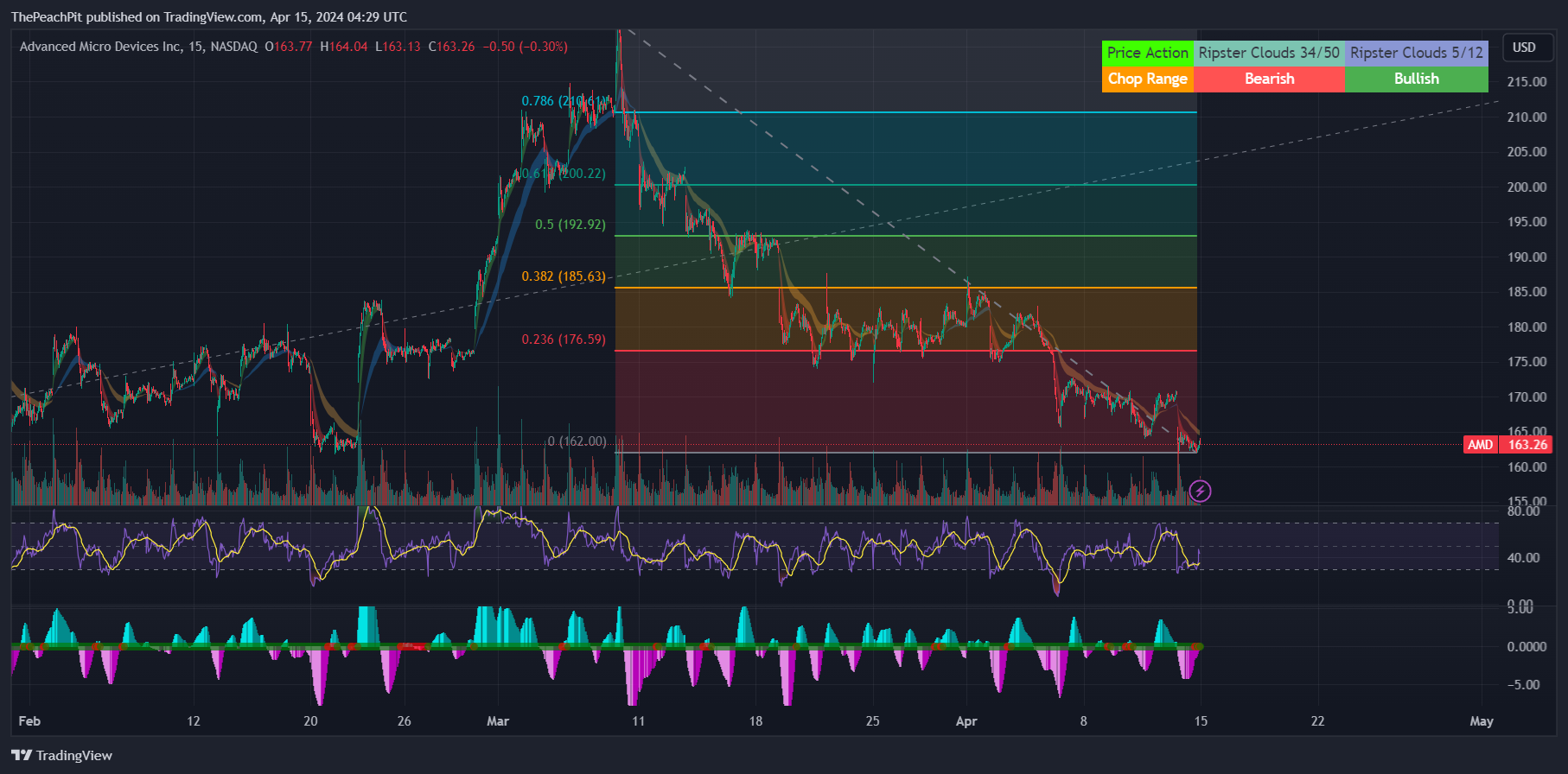

Speaking of AMD, the stock appears to be completing its retracement cycle before returning to a possible bullish run.

That said, the stock appears to be on a longer-term, downcycle trend and may experience just a short-term run-up before returning to a sell-off. Given AMD’s exposure to the PC market, I wouldn’t be surprised if their next earnings cycle is underwhelming. An earnings miss or any signs of a slowdown can drive the stock further down this path. If management confirms my AI-PC thesis, we may see this grand downcycle continue.

NVDA shares appear to be in a similar predicament at a less dramatic form. I expect the name to remain resilient in their bull run with minor retracements throughout the process. Given the backlog of AI server infrastructure outstanding, I do not expect a slowdown in growth anytime soon. The biggest negative catalyst that comes to mind is their dependency on Taiwan Semiconductor. Given the heightening geopolitical risk, I believe it is only a matter of time before a China/Taiwan skirmish takes place. Given President Biden’s verbiage towards the autonomy of the two nations as well as national security and trade risks involved in advanced semiconductor trade with China, I’m a little baffled as to how this will all play out. If China were to reclaim the Island, will NVDA still have the ability to produce chips in Taiwan? Will TSM have to redomicile to receive the fully agreed-upon CHIPS Act funds? Or is this some scheme to get TSM to build their fabs in the states, train up the staff, THEN allow China to invade, and force a sale of the new fabs? That would be one shady scheme that only a president of this caliber would choose to execute (do not take this as a political spin, this is purely a game theory exercise).

Lastly, my favorite name in the AI space, PLTR, hit a major inflection point down to the dot at the end of the trading week. Because I’m writing this Sunday night, I took the opportunity to publish a note on my Substack page regarding the trade for Monday’s trading hours. I expect that the stock will be experiencing a major breakout to the upside after a major pullback, so be prepared to load up on shares or call options.

Given their counter terrorist features and new partnership with Oracle, I anticipate some major international sovereign government contract acquisitions over the next few quarters. As outlined in my recent update, I anticipate this partnership to drive regional sales paired with margin strength as all of Oracle’s data centers are built with a modular design, allowing for seamless implementation of Palantir’s software. The regional housing of the datasets will also allow for the firm to more easily navigate local data privacy laws, which may drive a faster sales cycle. There are a lot of stakes in the flame that are just waiting to be stoked.

ThePeachPit Model Portfolio

Keep reading with a 7-day free trial

Subscribe to ThePeachPit to keep reading this post and get 7 days of free access to the full post archives.