ThePeachPit Model Portfolio Vol. VII

ThePeachPit Model Portfolio Vol. VII

This last week was certainly eventful with a strong swing in WTI oil prices, touching $87/bbl before settling within their previous range at $84/bbl. This week will be a busy one with March CPI & PPI readings coming out on Wednesday. Analysts expect higher inflation going into the print, which may solidify my thesis on no rate cuts this year. Bank earnings begin on the 12th with eyes on IB activity and NII.

I read an interesting headline that office vacancies are at an all-time high at 19.8%. I also consistently see headlines asserting that commercial banks are safe. These are rather conflicting statements, and my sellside suspicion is that someone wants to offload some equity positions and needs dumb money to buy up some positions. Unless those MBSs say “agency” next to them, I’d steer clear of the banks for now.

Core themes I’m playing into for q2’24:

- Natural gas recovery driven by domestic data center & international demand.

- Corporate AI wave of investments.

- Lackluster consumer electronics spending.

- Uranium retracement; looking for buy-in opportunities.

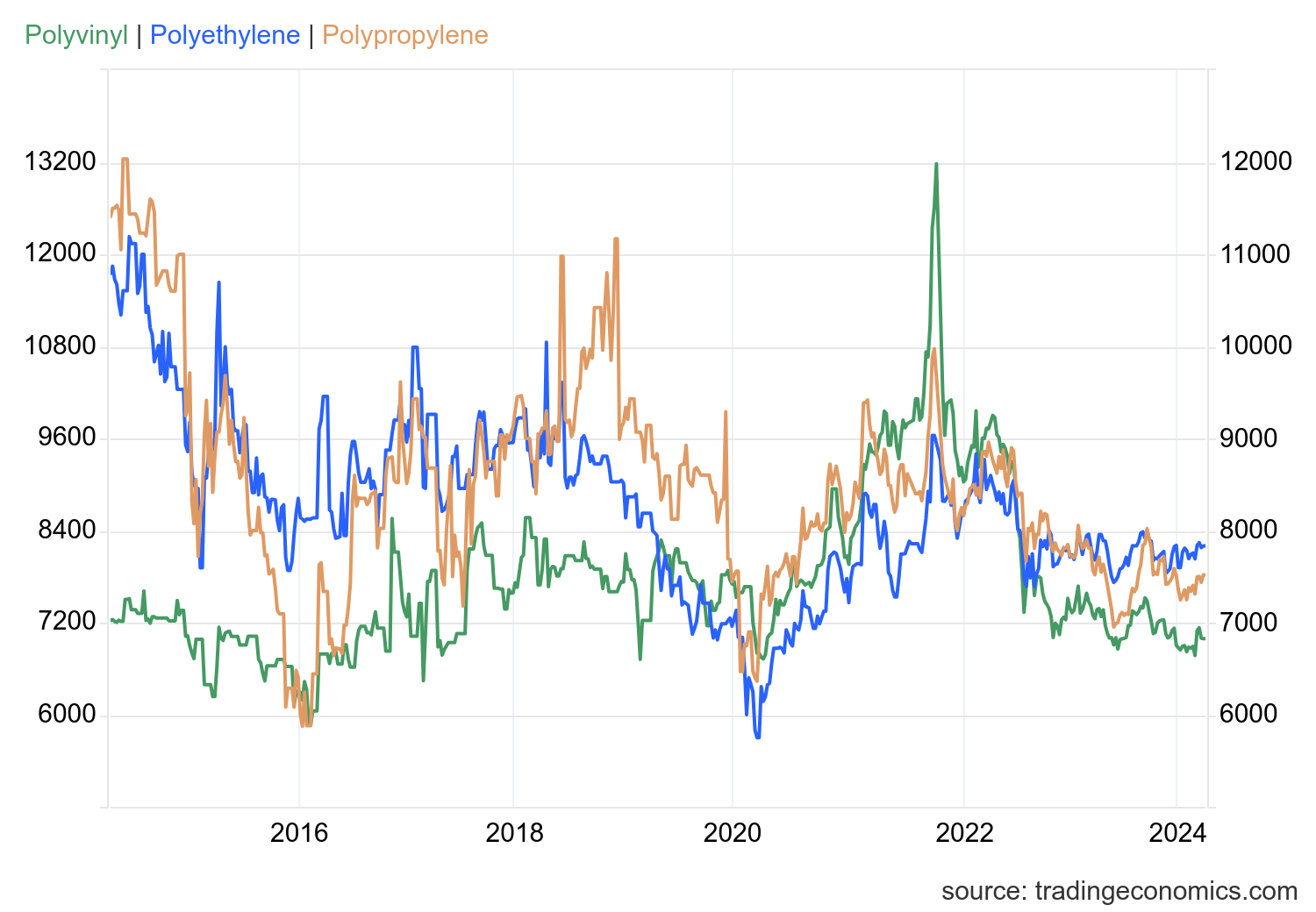

- Watching for petrochemicals recovery.

This was paired with a large swing in the S&P 500 to go counter to the price per barrel.

Much of the pricing was the result of tensions in the Middle East. I believe a lot of the more durable pricing action is the result of Russia cutting production as well as the country facing war-related destruction of refining facilities. Diesel exports from Russia are expected to fall by –16.4% for the month of April, which should ease global pricing pressures. The positive news is that Israel and Hamas are in discussions over a ceasefire, which may result in a more predictable market going forward. If discussions were to break down, I believe the S&P will be enroute to a further decline paired with strengthening oil prices to the $90s. Our IOC cohort responded positively through the end of the week of April 5th with the added pricing tailwinds. As we roll into q1’24 earnings season, I anticipate some strengthening across the cohort as y/y comps should be more appealing for eq1’24.

It has been reported that the Chesapeake and Southwestern merger has been delayed as a result of the FTC seeking more information regarding the deal. This isn’t necessarily atypical across the industry as the XOM/PXE and CVX/HES deals are also being analyzed with higher scrutiny by the agency. I believe this is all smoke and mirrors as the current administration makes an attempt to garnish stronger footing as we enter the next election cycle.

In steel, the United Steelworkers union rejected Nippon Steel’s appeal for takeover support, despite Nippon’s commitments to retaining employees through September 2026. As previously reported, I do not anticipate the US Steel/Nippon Steel merger to go through for a variety of reasons outside of the USW support.

This includes Trump’s anti-dumping tariffs enacted as a result of Nippon’s unfair practices as well as the integration of a foreign entity at a time of nearshoring. A merger between the two firms will make the US steel industry weaker and less competitive on a global scale. To bolster the industry, the initial merger between US Steel and Cleveland Cliffs would be preferential to compete on the global market.

As expected, investors are reacting negatively to the updates for US Steel, pricing in the deal as good as busted.

As laid out in my updated report covering Intel (link below), the firm released their updated corporate segmentation as they aim for better transparency between chip design and foundry services. The firm also laid out their 6-year plan as they ramp up their global foundries in anticipation of being the second-largest contract chip manufacturer by capacity. I expect this to be an uphill battle for the firm as third-party chip designers are expected to trust Intel with their next-generation IP. The biggest risk that can benefit the firm will be geopolitical-related, and given the administration’s stance on Taiwan/China, I believe that the hand may be forced. Be sure to read the full report found on Seeking Alpha.

Lastly, Taiwan was hit with their strongest earthquake in 25 years. This tragic event left a portion of the country’s infrastructure destroyed. As a result, Taiwan Semiconductor halted some of their production cycle as they assess any damages to their high-precision, chipmaking machines. It has since been reported that TSM’s facilities experienced minimal damage and that their EUV tools were not damaged from the quake and should be operational. Nvidia announced that they do not anticipate any supply disruptions as a result of the quake.

Catch up on all updates below

GSI Technology (NASDAQ: GSIT) 4/5/2024

Palantir (NYSE: PLTR) 4/4/2024

Coherent (NYSE: COHR) 4/3/2024

Dorian LPG (NYSE: LPG) 4/2/2024

CleanSpark (NASDAQ: CLSK) 4/1/2024

Occidental Petroleum (NYSE: OXY) 3/31/2024

Trades & Investments To Consider

Keep reading with a 7-day free trial

Subscribe to ThePeachPit to keep reading this post and get 7 days of free access to the full post archives.