I Swear It’s A Good Idea At Its Core (NYSE: ATKR)

I Swear It’s A Good Idea At Its Core (NYSE: ATKR)

This article covers a briefing on recent infrastructure-related legislation and a brief analysis of EGS-related investing. The investment thesis covers Atkore (NYSE: ATKR). Be sure to upgrade your subscription to read the full analysis.

It has been a bit over a year since the IRA was passed, and a lot has happened since then. Since the passing of the huge Inflation Reduction Act, the Federal Government has raised the minimum tax on corporate profits to 15% as well as a 1% excise tax on stock buybacks. These two corporate-related taxes are expected to raise over $300b over the next decade.

In addition to higher taxes, the private sector has $110b in new clean energy manufacturing investment in anticipation of receiving grants resulting from this act. Though it doesn’t appear any money has funneled through to the firms, it’s the thought that counts. As the Federal Government has proven, actions (or the lack thereof) are meaningless without positive public perception.

The Infrastructure Investment and Jobs Act provides nearly no color on investments made in new projects. What the program does provide is funding to states for distribution; i.e. there is not a centralized log of which firms actually receive funding.

The CHIPS Act appears to be in a similar boat in which funding has yet to be allocated for any semiconductor-related projects. In relation to this, the maximum grant received will be anywhere between 5-15% of the fab’s CAPEX. Digging a little deeper into the act, there is a requirement for firms that receive over $150mm to share any excess cash flows with the US Government upwards of 75% of the initial funding. In addition to turning over cash flows, the firm that accepts government funding MUST turn over documents of all underlying technology and manufacturing processes to be utilized in the facilities. The program also restricts any shareholder benefits such as buybacks and dividend distributions.

The Wall Street Journal reported Monday that three firms set up to take government-guaranteed loans, Li-Cycle Holdings, Plug Power, and NuScale Power, are each either delaying or canceling projects due to “ballooning construction costs and higher interest rates.” What it came down to was the chicken or the egg – government-guaranteed loans must be syndicated by banks, and qualifications for tax credits don’t show their effects until after the facility is in production. I reported some serious criticism on ThePeachPit earlier this year regarding the government’s questionable investment history when it comes to previous, similar programs. I discussed both historically failed projects as well as criticism for selecting Li-Cycle, a lithium battery recycling company that burned through 75% of its cash reserve in the last year as profitability still remains a moonshot.

As you can already tell from previous issues of ThePeachPit, I oftentimes don’t go after the leading-edge trailblazers. As stated in my analysis on Exxon, never invest in the first mover; invest in the slow-moving ship that calculates every turn. These firms tend to be more durable and focused on profitability as opposed to growth at all costs. As Peter Lynch had coined, buy companies that experience growth at a reasonable price (GARP).

As one may also discern, I was very wrong in the timeliness of these US Citizens’ funded programs as issued by our employees, the US Government. These poor assumptions were baked into my investment thesis for Quanta Services (NYSE: PWR) and Argan (NYSE: AGX). Though each company has experienced a nice uplift in their share price since publication, the rationale didn’t quite make it to the cash flow statements. Despite each company experiencing strong operational growth, I was still wrong with my underlying growth thesis. Nevertheless, I wasn’t necessarily wrong on the rationale, just on the timing; so as Jim Carrey said in Ace Ventura, “If I’m not back in five minutes, just wait longer!”

Before I get into this week’s investment thesis, I want to cover a huge win for Wall Street. Monday’s Wall Street Journal issue came with a treasure trove of articles covering areas that ThePeachPit has either reported on or criticized since beginning publication a little over a year ago. As reported, for the first time ever, more ESG funds are either closing or removing the ESG nameplate than ESG funds being created. Through a series of malinvestment, sales and marketing ploys, and potentially pure cash grabs for faulty businesses, the ESG-related publicly traded companies have underperformed to the point that these high 1.5-2.0% managed funds are calling it a day! Big win for us old school investors!

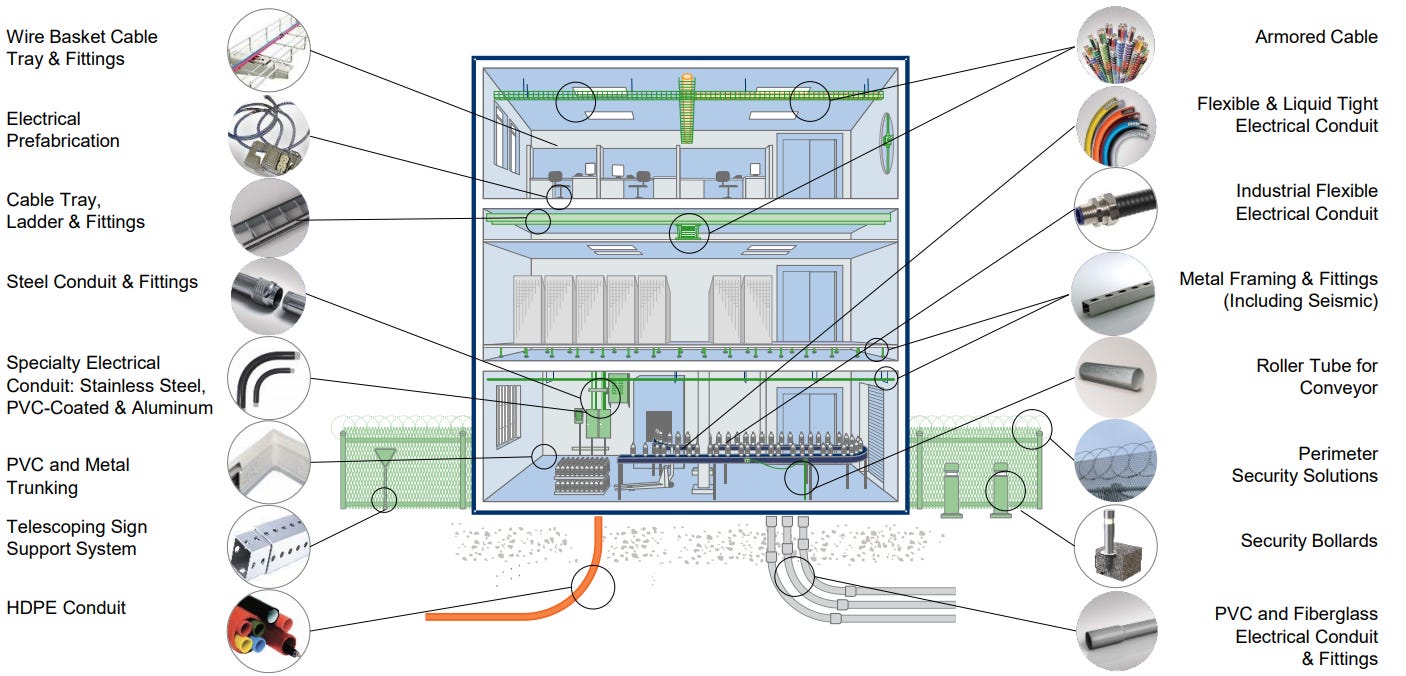

This week’s investment analysis covers a cyclical company in the industrials space, Atkore (NYSE: ATKR). Atkore is in the business of manufacturing the protective conduit for cables used in a variety of non-residential applications, such as datacenters, telecommunications, electric power, and transportation, as well as cable management systems. Much of their sales derives from new builds as well as renovations and modifications to older facilities. Despite the slowdown in commercial real estate, other areas of real estate remain under development, including telecom/datacom and electric power.

This is one of those boring companies to keep an eye on. Though I’m not currently recommending a BUY recommendation just yet, I will be updating my recommendation come the end of CY1h24 as Atkore resolves the downcycle of their industry. Challenges faced in FY23 included destocking, cost/revenue differentials in which the price of products sold declines before the cost for the same products, and challenges as mentioned in my briefing up above relating to the timing of funding relating infrastructure bills in place. Management did disclose verbiage that projects are shovel-ready and just awaiting funding. Though I’d like to say I have faith in the speediness of funding, given the challenges faced by Li-Cycle and Plug Power, I find it hard to believe many of the projects will break ground. This higher interest rate market has made financing costlier and will significantly shift the curve for project accounting (lower IRR/NPV outlays).

There are some factors that I do like about Atkore that makes them a very viable future investment candidate. The first is the old Peter Lynch adage, boring is better. The company is very well established, in a GDP-tracking growth trajectory, and isn’t chasing the puck in shifting markets. They’re very good at what they do and are slowly steering the ship through M&A. The second is their valuation. The firm is valued at $5,526mm, $375mm of which is attributable to net debt. The firm holds very low debt levels with EBITDA covering their total debt burden by 2.69x. The firm also trades at a relatively low valuation at 5.5x EV/EBITDA with a free cashflow yield of 11%. Lastly, Bill Waltz, Atkore CEO, announced the initiation of a dividend come q1’24 (0.30-0.35/share, or an annualized yield of 0.92% - 1.07%) on top of their share repurchase program with $300mm remaining. With these virtues, I provide ATKR a SELL recommendation along with the recommendation to dollar cost average shares throughout 2h24 as Atkore undergoes the tail end of the cyclical downturn.

In all honesty, I’m quite surprised this company has remained off of my raider for this long. Given their significant growth over the last few years without racking up significant amounts of debt or issuing equity (in fact, quite the opposite), this firm has grown from generating $250mm in operating cash flow in FY20 to $808mm in FY23.

Keep reading with a 7-day free trial

Subscribe to ThePeachPit to keep reading this post and get 7 days of free access to the full post archives.