Earth, Wind, and Fire: Nuclear, Wind/Solar, and Natural-gas Fired Power Plants (AGX)

Earth, Wind, and Fire: Nuclear, Wind/Solar, and Natural-gas Fired Power Plants (AGX)

There has been a lot of news coming across the tape relating to infrastructure and power transmission. Some of the more well-known pieces include the Texas freeze in 2021 that left much of the great state without power for a little over a week during one of the harshest winter freezes the state has seen in a generation. Much of the discussion revolves around who is to blame for the lack of power. Was it corporate greed, sky-high natural gas spot prices, or the dysfunctional power regulatory branches, ERCOT and PUCT? To cut to the chase, there were multiple factors that came into play; however, my conclusion revolved around PUCT and the mislabeling of critical infrastructure that reallocated much needed electricity away from the power producers to the homes, or clients of the power producers. In other words, Instead of providing power to continue producing more power, PUCT attempted to take charge and inevitably turned off the power for vital gas pressure pumps that led to the inability to move natural gas across the pipeline infrastructure to the producers.

Another great example resides on the other side of the world, in California, a geography that is prone to extreme dry heat and rolling blackouts. In late 2022, California officials had declared a statewide grid emergency due to an extreme heatwave, adding pressure to the already flimsy grid. Due to a decades’ long drought, the failure of the state’s hydroelectric power plants, which account for roughly 10% of the state’s electricity, added additional pressure to the grid. Through rigorous, and misguided, ESG state policies, natural gas-fired power plants have either reduced capacity or closed as the state turned its sights to less energy-efficient solar and wind to power homes and businesses.

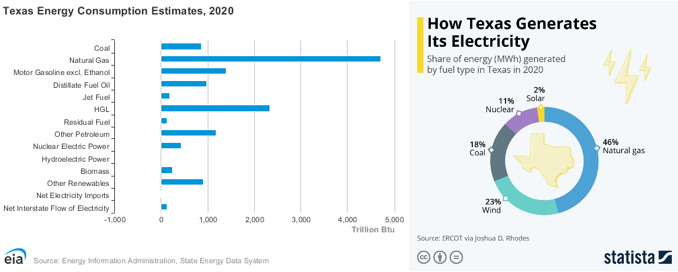

In a 2021 report by California’s Energy Assessments Division, California’s grid has been significantly weening off of fossil fuels. Natural gas currently accounts for 37.9% of the total power mix while solar and wind account for 14.2% and 11.4%, respectively. Power capacity is so bad that California is forced to import roughly 30% of their power from surrounding states to accommodate for insufficiencies. Below are two charts outlining power consumption on the left and production on the right.

Texas, on the other hand, depends more heavily on fossil fuels, with natural gas and coal accounting for 46% and 18% of electricity produced. As compared to California, Texas’s renewables account for 25% of the grid, as opposed to 33.6%. More importantly, Texas’s grid runs independently and does not import any electricity.

Texas, on the other hand, depends more heavily on fossil fuels, with natural gas and coal accounting for 46% and 18% of electricity produced. As compared to California, Texas’s renewables account for 25% of the grid, as opposed to 33.6%. More importantly, Texas’s grid runs independently and does not import any electricity.

Much can be said about the resiliency of renewables. Like the batteries found in electric vehicles, renewable power sources really only work under certain conditions and may not produce at optimal rates even during perfect conditions. The obvious examples include the necessity of sun for solar panels to function and the wind must be blowing for the blades on a windmill to rotate. Extreme heat and cold weather can also have disadvantageous effects on windmills from properly functioning. To make matters worse, the grid that connects all this power generation to our homes and offices isn’t built for intermittent energy sources; i.e. fossil fuel-fired power plants produce a constant flow of electricity while solar only produces electricity during the day, contingent on sunny skies. This intermittency adds additional stress to the transmission grid that may cause more harm than good.

Reliability and transition from one source to another upon failure will need to be more heavily considered when transitioning to renewables. According to MIT research, timescales are affected to the extent that rather than having minutes to hours to coordinate backup capacity, the amount of time to transition from renewables to fossil fuel backup capacity will be narrowed this down to seconds.

Batteries have been making waves in recent years in providing stored energy after dark. Though we’re still in the early innings of batter development, some strides have been taken in the science behind iron-air batteries. Despite batteries providing backup capacity to manage intermittency, the Director of Reliability Assessment and Performance Analysis, John Moura of NERC, or the North American Electric Reliability Corporation, blatantly stated “Batteries aren’t going to do it, and we’re going to need a backup fuel for wind and solar. So, this is important to invest in.”

Scaling battery storage has been a major challenge to overcome. Vistra Corp (VST), a major electricity generator and retail power provider had initially sought to resolve this problem in California with their Moss Landing battery storage system. At the end of 2021, Vistra had just completed an expansion of their 400MW battery storage facility to help alleviate the intermittency of power flow on the grid. Despite early success, operational challenges in the facility would arise due to the batteries igniting, creating a smoke hazard in the facility. Vistra was forced to shut down the facility shortly after completion in February 2022 due to these safety hazards.

This isn’t an isolated incident. PG&E experienced a fire in their battery storage facility back in October 2022. There have also been several fires in Arizona’s battery storage facilities, one in Arizona Public Service’s facility back in 2019 and another in April 2022 at the Dorman battery storage system.

There are a variety of causes for these facilities to go up in flames. Marsh Commercial, an insurance broker that backs facilities such as these, explains that issues can derive from defects and damage in the lithium-ion batteries due to excess heat in the facility, leading to fires or explosions, the emission of hydrogen gas from lead-acid batteries creating similar risks, and control system failure leading to overheating and fires.

Batteries are in a unique position that comes with its own challenges across renewable energy, economics, and geopolitics. Batteries require energy-intensive mining operations to gather the minerals out of the earth. These mining operations require a tremendous amount of diesel fuel and heavy machinery to extract resources from the ground. Many of these mineral deposits reside in high-risk regions that may lead to the exploitation of the local residents. Economics also don’t quite align, which I will further get into, given the lower energy efficiency as compared to traditional resources.

According to an article in S&P Global, “At the end of 2021, the European Chemicals Agency's Risk Assessment Committee agreed with French proposals to classify lithium carbonate, lithium hydroxide and lithium chloride as Category 1A reproductive toxicants, as they may damage fertility, unborn children and harm breastfed children.” Accordingly, Category 1A means that this chemical is of “high concern” and restrictions of use should be considered. The challenge imposed would lead to significant restrictions on the mining, refining, production, and recycling of lithium salts in the European Union. As a result, the European Commission recommended that these lithium salts NOT be classified as 1A substances because it would create further challenges in Europe’s lithium value chain and make it near impossible for the EU to achieve their Green Deal objectives.

There is hope for battery storage, however. Form Energy, a Massachusetts-based energy company, has developed breakthrough battery technology using iron. Rather than providing backup storage capacity lasting a few hours, their iron-based battery is suggested to last for 4+ days. There are tradeoffs when building batteries with iron as opposed to lithium. Iron-based batteries are much larger and heavier than lithium-ion batteries. Iron batteries also contain moving parts that would put a vehicle at risk if implemented. The purpose for iron batteries isn’t necessarily meant to replace lithium-based batteries but rather be used as back-up capacity for the grid.

ESS Tech, Inc. (GWH) is also heavily invested in the technology development for iron-based battery storage. Each of these shipping container-sized batteries is capable of powering 34 homes for 12 hours. ESS is also in the process of developing even larger batteries to solve the issue of intermittent energy sources. This sounds like a great opportunity; however, it costs roughly $105mm for ESS to produce $900k in revenue. It may be a bit too early to critique their current financial position when considering the long-term growth potential. My biggest concern is that the ESG wave came and went. The hype between 2020-2022 drew eyes to the space only to be disappointed by the results. Why didn’t more customers flock to ESS during this time? With only $5mm in accounts receivable, it’s challenging to buy into the hype.

To add a little salt to the wound, Grizzly Research issued a short-sell report on ESS Tech back in December 2022 which resulted in a lawsuit against Grizzly Research by ESS Tech. Lawsuits don’t typically result from short-seller reports unless the statements made in the report are true.

To read more about the makeup of electric vehicle batteries, please follow the link, Tough Roads Ahead: Navigating Through A Challenging Automotive Market (substack.com)

I believe one of the biggest challenges when it comes to energy transition is energy transmission. Energy security and reliability need to be the top priority in transitioning from carbon intensive energy to more “green” renewable energy sources. There is a time and a place for renewable energy; however, the idea of phasing out fossil fuels and nuclear power generation before this technology is more efficiently developed creates a significant hazard to the security and reliability of our grid and economy.

To cite research from Goehring & Rozencwajg, “renewable energy production is relatively inefficient as compared to traditional fossil fuels. “ Low load factors and “buffering” of intermittency results in poor “energy return on energy invested” (EROEI). As much as 25–60% of the energy generated in a renewable system is consumed internally, compared with 3% for a modern gas plant.” – G&R

To think that we, as a society, are moving towards less efficient energy production is an incredible phenomenon. Not only are they less reliable sources of energy, they cost more and the decommissioning process creates even more hazards. Wind turbine blades cannot be recycled and the cost of repairing/replacing the blades has led to straight retirement of the turbines. According to Bloomberg, the blades must be cut into three pieces using a diamond-encrusted industrial saw before being strapped to a tractor-trailer to be hauled to the local landfill. Another haphazard to note is that in late 2022, a windfarm in Germany was dismantled to expand an open-pit coal mine. It’s clear that the run of fossil fuels isn’t over, and in fact, will be expanding for the next decade.

There will be the need for replacement capacity, however. The EIA estimates that 15.6GW of capacity is going to be decommissioned throughout 2023. Retired coal-fired power plants are going to account for 8.9GW while 6.2GW will come from retired combustion turbine natural gas power plants. The EIA goes on to state that the natural gas-fired power plant uses older steam and combustion turbine units that are far less efficient than modern combined-cycle natural gas-fired power plants. Three of the natural gas-fired power plants reside in California.

Looking out to 2029, the EIA expects the retirement of nearly 25% of coal-fired power plants for a total of 9,842MW of capacity. Most of these retired coal plants will come from Michigan, Texas, Indiana, and Tennessee. Historically, most of the retired coal plants have been displaced with natural gas. Looking forward to the next 6 years, it is likely that this retired coal capacity will be replaced with natural gas.

In early 2022, the EU ran into challenges in securing natural gas due to Russia’s state energy company, Gazprom, gradually reducing natural gas flows to Europe as the war between Ukraine/Russia progressed. Eventually Gazprom shut off all gas flows through Nordstream I (not to be confused with Nordstream II, which was never approved for production by the Dutch government). As the concern for the coming winter heightened, the EU took drastic measures in limiting electricity usage by residential and commercial buildings and limited manufacturing. Spot prices for natural gas went to the moon during this period as the EU scrambled to replenish their storage capacity before winter. Though natural gas has come back down to earth, spot prices still remain elevated compared to historical averages.

Despite the EU overcoming this short-term challenge, it didn’t quite solve the underlying problem; renewable resources are not dependable and the necessity of natural resources and nuclear to produce energy is vital to the greater good of society. This challenge actually flipped the EU’s stance on natural gas and nuclear energy from commitments to ban these two resources to now including them in their ESG approved list.

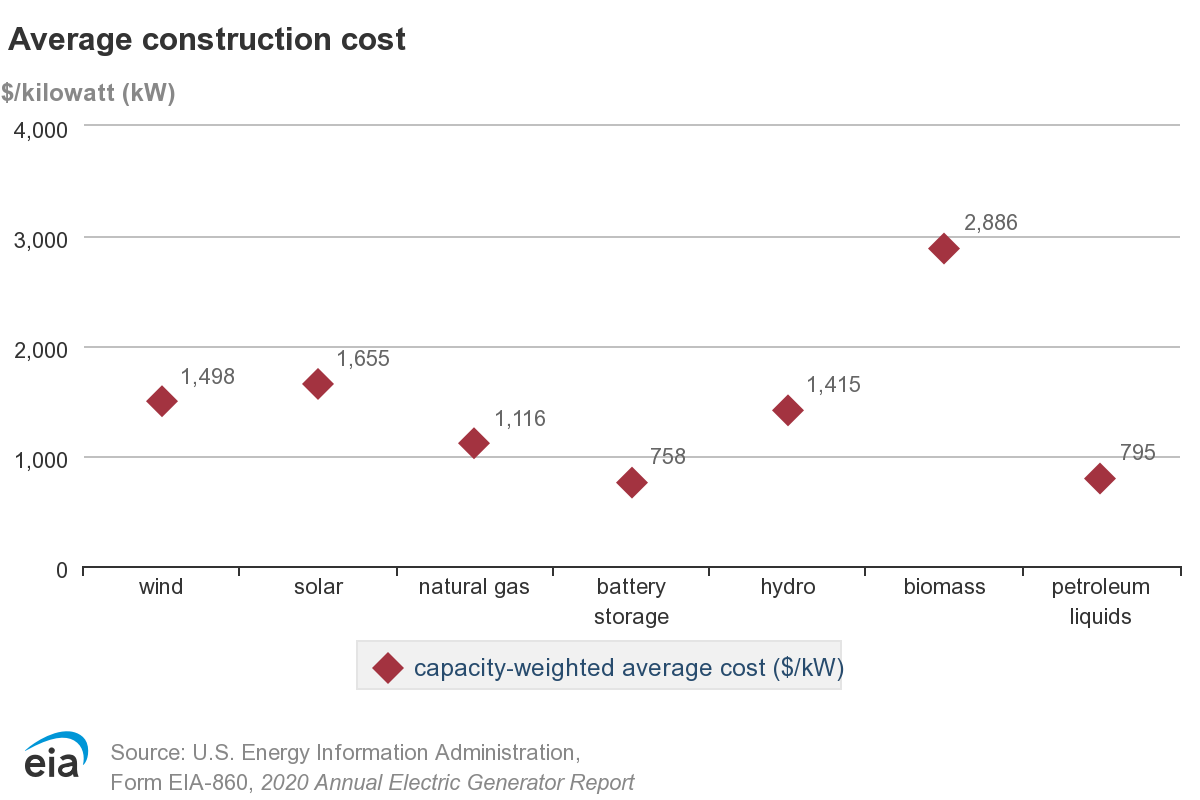

When comparing electric transmission, it’s clear that renewables aren’t quite competitive to traditional resources. Considering the costs to construct capacity, new solar capacity costs roughly 1.5x as much as natural gas, and that’s not including the cost of backup battery storage capacity. To get more granular, it is suggested that natural gas will be used for back-up capacity for solar and wind; so however you cut it, the cost to utilize solar and wind will potentially need to include battery capacity and natural gas as back-up capacity. I’ll let the reader do the math for this one.

Inflation Reduction Act

The inflation Reduction Act (IRA) was passed on August 15th, 2022 in an attempt to expand US manufacturing, technology R&D, and improve energy security & power transmission modernization. In reviewing the Department of Energy’s expansionary program, it’s challenging to presume much of the financing will reach the right companies.

Out of curiosity, I went to the DoE website to see what companies are sourcing these loans. Ly-Cycle (LICY), a Toronto, Canada-based “company”, will receive a $375mm loan to develop a ground-breaking lithium-ion battery materials recycling facility in Rochester. According to their filings, the loan will track the 10-year US treasury rate at the time of each advance for the loan. EX-99.1 (sec.gov)

It’s hard to tell if these are going to be the standard terms for future loans. If this is true, the IRA may open the door to a flood of guaranteed loans to be allocated to risky, and even at risk companies. Given that the 10-year note has ranged from 4.25% in October 2022 to now 3.58%, banks issuing investment-grade rates may be less than ideal for risky businesses. Oh, by the way, guess who’s on the hook in the instance of default. It certainly is not the banks. It will be the taxpayers.

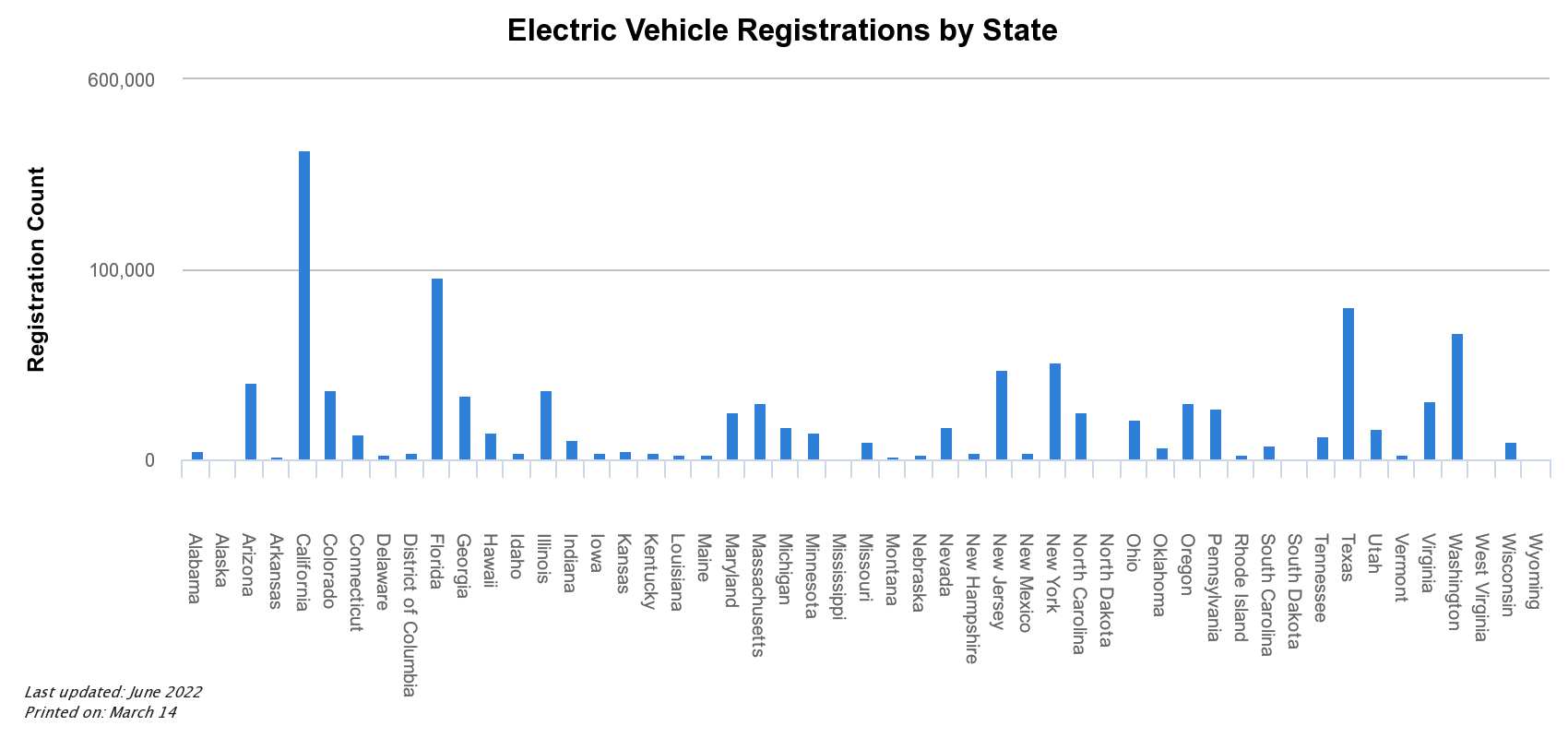

Briefly going back to Ly-Cycle, what I found most interesting about this was the geographic location of the plant. Given that the majority of registered electric vehicles reside in California, followed by Florida and Texas, it doesn’t make much sense to place a battery recycling plant way up in western New York. Given that a lithium battery in an EV weighs roughly 1000-2000lbs, or 50% of the vehicle, it’s challenging to make sense of shipping batteries all the way from the southern regions of the US all the way up to New York. In my recent short-sell recommendation for SmartSands, I outlined the financial performance risk of higher transportation costs of shipping frac sands across basins. The Bullish/Bearish Case In Energy (SND) - ThePeachPit (substack.com) Good thing we still have diesel-powered locomotives! We certainly will need to modernize our country’s infrastructure to support these government-financed projects.

To rub salt in the wound, Ly-Cycle has yet to generate an operating profit since inception. I’m not sure where their money to finance this loan will come from, but hopefully management figures it out.

To breakdown the IRA’s loan program, the Innovation Clean Energy Loan Guarantee Program will provide $40b in loan guarantees under section 1703 of the Energy Policy Act of 2005 and $3.6b in credit subsidies to support the cost of clean energy technology projects, including fossil fuels and nuclear energy. This also includes critical minerals processing, manufacturing, and recycling. The Energy Infrastructure Reinvestment (EIR) Program will appropriate $5b with a loan cap of $250b that will guarantee loans to projects that will retool, repower, repurpose, or replace energy infrastructure that has ceased operations, or enable operating infrastructure. This money will go to companies to avoid, reduce, utilize, or sequester air pollutants or anthropogenic emissions of greenhouse gasses.

The Advanced Technology Vehicles Manufacturing (ATVM) direct loan program is intended to remove the $25b cap on the total amount of ATVM loans as established under the Energy Independence and Security Act of 2007. This portion will provide up to $3b credit subsidies and up to $40b in loan authority. These loans are intended for vehicle and component manufacturers for medium- and heavy-duty vehicles, locomotives, maritime vessels, offshore wind vessels, aviation, and hyperloop.

The last portion is the Tribal Energy Loan Guarantee Program (TELGP). This piece increases the availability of loans from $2b to $20b under the Energy Policy Act of 1992 and is intended to direct loans to the Alaska Native Corporation for energy development.

There seems to be a wide variety of programs for which this bill will open the door to new financing. Reviewing the LPO website, there are currently 8 companies that have repaid their loans in full and 17 still outstanding under Title 17 since the Obama-era recovery act. Many of these loans were geared towards solar, wind, and the automotive industry. There are a few recognizable names on the list, namely Tesla and Ford. There were two loans issued in mid-to-late 2022, one for $102mm to Syrah Vidalia, an Australian-based graphite mining company with operations in Louisiana, and the other for $2.5mm to Ultium Cells, a private lithium-ion battery cell manufacturer in Tennessee. Graphite has a variety of uses in developing batteries and nuclear energy. Given the public interest in modular nuclear reactors, this may be an interesting area to watch.

Despite the successes of a few loans, there are a number of less-than-successful projects. Bankruptcies ranging from 2011-2013 include Fisker, Crescent Dunes, Abound Solar, and Solyndra, each of which received loans from the DoE and inevitably defaulted. Fisker had previously filed for bankruptcy in 2013 after burning through $1.4b in private investments and taxpayer-funded loans. Fisker has more recently reemerged through a SPAC, raising around $1b for a valuation of $2.9b. History doesn’t repeat itself, but it sure does rhyme.

To summarize the IRA, it is challenging to see any improvements to responsible financing. If anything, this will perpetuate the equity craze in 2020-2021 where startups raised capital through equity sales by going public through SPACs. The only difference is that ignorant, speculative traders aren’t going to be on the hook. The US taxpayers will be responsible for footing the bill for loan defaults and may lead to further inflationary pressures. That said, this may also create opportunities for companies that will be contracted to build these facilities. That brings us down to the overarching point of this newsletter.

Investment Thesis

In reviewing this week’s investment idea, an array of new power plant projects came up. Argan, a global EPC services company, is responsible for designing and building out these power plants. A few major projects completed in 2022 include a combined cycle gas-fired power plant and a wood-pellet-burning power plant in the UK. Their backlog of projects are primarily gas-fired power plants across the US, UK, and EU, totaling roughly $700mm. Between traditional fossil fuel-fired power plants and wind and solar farms, I believe Argan will experience a huge upswing throughout the next decade of power transmission innovation. Between building out natural gas capacity and renewable capacity, Argan has a lot of opportunity to grow their cash flow potential.

Argan (AGX)

Argan, Inc. is an engineering, procurement, and construction (EPC) services across the power transmission industry. Founded in 1961, Argan has been responsible for constructing over 400 installed turbines with over 65GW of capacity since inception. Through their subsidiaries, AGX designs, constructs, and services power plants, and provides enterprise telecom services and industrial fabrication services. Argan’s operations runs under four main subsidiaries, Gemma Power Systems (GPS), Atlantic Projects Company Limited and Affiliates (APC), The Roberts Company (TRC), and Southern Maryland Cable (SMC). Their primary revenue generator resides in their power and industrial services units, which provides EPC services for power plants.

Much of their revenue is derived from EPC services in building out new power capacity across the Midwest and East Coast of the US, Ireland, and the UK. Their business has historically been driven by building out natural gas capacity but has more recently diversified across renewables and hydrogen fuel. One of their biggest projects is the 1,875MW natural gas-fired power plant in Guernsey County, OH. This plant is deemed the largest single-phase, gas-fired power plant construction project in the US. One of their projects under development is the monster Maple Hill solar facility, a 480-acre, 235,000 photovoltaic module solar facility that produces a total of 100MW of electrical power located in Pennsylvania.

What I find amazing is that a nuclear plant takes ~640-acres to produce 10x the electric capacity as the solar farm. We probably don’t need that extra land anyways.

Power services is the primary revenue driver, accounting for nearly 80% of their business. This comes to no surprise given the growing interest in energy security and the reliability of the grid. Whether it is a result of extreme weather or geopolitics, the necessity of reliable energy is vital to protect the integrity of our economy. Given the drive to bring home manufacturing across all industries, especially the semiconductor industry, we cannot risk anything less than dependable power transmission.

Despite recent revenue declines, the company has weathered the storm and managed operations throughout C19. Considering the vast opportunity in modernizing the grid, Argan is in a unique position to experience significant growth throughout the next 10-12 years. Argan’s shares is currently trading at a deep discount to its peers and has room for valuation expansion on top of growth. For more information on my investment thesis on Argan (AGX), please visit SeekingAlpha for the full report.

Keep reading with a 7-day free trial

Subscribe to ThePeachPit to keep reading this post and get 7 days of free access to the full post archives.