Build Bigger and Better (NASDAQ: TRMB - PT $83)

Build Bigger and Better (NASDAQ: TRMB - PT $83)

As the economy churns, the Fed burns. Inflation has experienced quite the trip over the last year, peaking at around 9% around this time a year ago, falling back down to earth to 3% growth in June, off of just under 5% in May. Though that’s hardly a win given historical levels in the US, that is substantial progress given the Fed’s aggressive rates tightening program.

There are many theories that go into the rollercoaster ride experienced throughout the last few years. Some take a more monetary/political approach while others take a more economic-based supply/demand approach. I fall into the latter on the basis that supply-side economics drove much of the supply constraint. One perspective to consider that often gets overlooked, is that the halt in production during 2020 had a greater effect to supply constraints than most give credit for, followed by a huge spike in demand for materials in 2021, leading to a disjointed balance in the supply/demand equilibrium that led to a huge run-up in the prices for materials. Naturally, this price increase in the producer price index trickled down to the consumer price index, leading to much of the inflationary pressures experienced in the last year. Fast forward to today, much of this production imbalance has waned, leading to more normalized prices. The challenge consumers face now isn’t that the pricing pressure has normalized, but that the law of sticky prices in which we as consumers are comfortable with the higher prices, and higher prices will persist.

Using the Bloomberg Commodities Index (BCOM) as a proxy, it’s pretty clear that the aggregate commodities index has pulled back significantly from its peak in May 2021. This has significantly relieved much of the pressure on PPI.

The next chart shows PPI & CPI stacked back-to-back. Considering the BCOM path and the path of PPI, it’s clear the pricing pressure for producers has significantly been relieved but isn’t quite back down to pre-pandemic levels.

Despite this drastic turn of events, we’re still not out of the woods given how much of the inflationary effects aren’t “sustainable”; meaning, much of the events that drove inflation was from a hard stop and a hard start. What I’m trying to infer isn’t necessarily an end to inflation, but when the dust settles, what the terminal price level commodities will be pulled towards. Year-to-year rates of change is how inflation is typically quoted, but negates any real effects on the consumer. What is often overlooked by the media and what is felt by the consumer is the nominal level of prices. This is the figure that’s driving much of the changes in shopping habits for consumers and pushing more and more consumers into deeper credit card debt. Most people like getting a deal on goods, but we seem to be stuck with paying more for less.

As one can discern, when producer prices decrease, consumer prices kinda/sorta but not really follow suit. It’s similar to the fascination analysts have with Sherwin Williams. As the price for propylene increases, the price paint is sold at increases. As the price of propylene decreases, the price of the very same paint remains at the same elevated level. After all, most consumers don’t typically monitor the input costs for their products. Despite the information being very public, most just don’t seem to care.

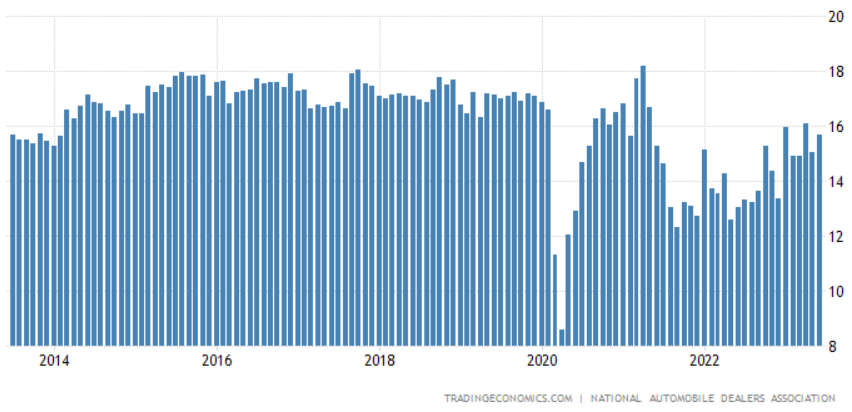

In other news, the automotive industry has been taking a turn in recent days. The Manheim Used Vehicle Value Index has declined two consecutive months into May with an 11% year-to-year decline. In just as good of news, the WSJ reported on July 5th that new vehicle sales improved by 13% in the first half of 2023, with industry-wide sales reaching 7.7mm new vehicles sold. Automotive manufacturing is certainly back into the swing of things. According to UBS, production is expected to outpace consumption by 5% in 2023, leading to an excess of 5mm vehicles that may require dealership deals to offload. Though despite this marginal development, vehicle manufacturing is still off from its pre-C19 levels. There’s a lot of rightsizing that needs to take place in this industry. For the most part, many dealerships oftentimes resorted to cutting deals to offload excess capacity of vehicles. The reset that C19 led to actually helped dealerships improve margins and sales while resorting less and less to cutting deals with buyers.

This somewhat coincides with an investment thesis I had back in early 2021 for automotive dealerships, such as Asbury (NYSE: ABG) in which reduced inventory of new vehicles will drive up margins, which it certainly did. Reviewing ABG’s Q1’23 results, it appears this strategy has been played out with same store vehicle gross margins declining -2.02% Y/Y. Group 1 Automotive (NYSE: GPI) experienced a similar decline of -5.7%. Given these two datapoints, let’s look at the aggregate data as provided by the St. Louis Federal Reserve.

Well, prices do appear to be rolling over, but much too soon to come to any meaningful conclusion. My expectation is that prices will remain elevated for the time being and may begin to slump throughout 2024 as more and more consumers and businesses face a harder debt landscape.

The last data point worth mentioning in this note before I segue into my stock idea is focused in real estate construction, primarily in the industrial space. The WSJ reported on July 3rd that spending on construction of manufacturing facilities increased a whopping 76.3% year-on-year in May. Much of this effort can be attributed to the passing of the Inflation Reduction Act (IRA) and the CHIPS Act, which I have heavily researched in previous notes.

Aside from the CHIPS Act, this progress can be attributed to the insourcing of manufacturing processes away from China in an attempt to domesticate, shorten, and optimize the manufacturing supply chain of semiconductors and other materials. How effective this will be when all is said and done is to be determined; however, for now, the important factor to focus on is the construction activity.

Much of the activity is derived from the necessity to bring electronics manufacturing home stateside. In fact, according to Deutsche Bank, 18 new semiconductor foundries are in the process of being constructed across the United States. What seems to be overlooked is staffing. Who is expected to run these highly specialized machines that require microscopic precision? Given the fact that much of the foundry work has been outsourced for well over 2 decades can insinuate that the US doesn’t have the trained personnel to manage these fabs. A+ for construction jobs. C- for effectiveness.

Regardless, the US Treasury is giving us a pretty clearcut view on construction growth for the technology industry. This level of spending hasn’t been seen in my lifetime and maybe many of my readers’ lifetimes.

Accordingly, the Department of Treasury suggests that public spending on roads and bridges has experienced an increase in spending by 13% this last year, with major projects projected to expend $110b over the next 5 years. This can be rebuilding/repaving existing roads, developing new roads, and anything in between. Given the continuation of growth in residential real estate, renewable energy, and manufacturing plants, the necessity for more roads shouldn’t come to much of a surprise.

That’s a lot of money to be spent on infrastructure projects in the coming years, which brings us to my investment thesis on Tremble (NASDAQ: TRMB). Trimble is in the business of creating usable data with real world applications for construction, engineering, agriculture, and utilities, amongst others. Their products take data collected from their analytical tools like scanners, channels the data to the home office through a cloud-based application, and creates usable workflows for further analytics and project development. Their largest business unit is their buildings and infrastructure, which includes a wide array of applications, including a 3D modeling application for designing entire buildings all the way down to the wire.

Other applications involve transportation management which uses a combination of geospatial data and on-road data to optimize routes and minimize downtime for drivers. Their agriculture arm also uses geospatial software for automating the entire farming cycle, including crop harvesting and weed elimination. In short, Trimble is able to cross-sell and repurpose various software applications across different industries to maximize utilization of their products.

Reviewing their financials, I’m pretty on the fence with this company. Growth seems to have stalled out this last year, FY22, with FY23 projected to be relatively flat at 5% topline growth. One key point management disclosed in their recent earnings call was that margins should be expansive for the duration of FY23 given that the majority of their growth investments are in place and should have the flexibility to pull back on spending. In fact, this will result in some extraordinarily robust EBITDA expansion, growing from last year’s 19% to 30%.

There are a lot of macroeconomic factors that will be going into Trimble’s operating performance going forward. The first that comes to mind is the high interest rate environment that we’re presently in. With the federal funds rate sitting above 5%, the highest it has been since q3’07, there may be some hinderance in customer growth. For example, with a global economy teetering on the downcycle, industrial projects may be postponed or scrapped. Whether this happens is to be determined, especially given the three bills passed in the last few years, as referenced above, the IRA and CHIPS Act, as well as the Build Infrastructure Bill, or the Back Better Bill. Each of these have components that will benefit customers of Trimble, and in turn, benefit Trimble.

One concern is the flagging demand for commercial real estate (CRE). With vacant buildings comes vacant demand for new builds. The saving grace here will reside in the multifamily space, which appears to be relatively mixed. According to Arbor Realty Trust, new builds hit its highest level since 1986 with new construction starts reaching 529,000 new multifamily units.

The challenge will be going forward coming off of a banner year, with estimates of a 28% slowdown before stabilizing in 2024. Despite this large pullback, this level of a slowdown should be expected as the greater economy slows, the commodities prices, as outlined above, settle at an elevated level, and as the levels of supply/demand normalize.

The “Build Back Better” Infrastructure bill that was put in place at the end of 2021 reserves $1.2b for infrastructure investment over the next 5 years. The breakdown is quite robust, with $240b being allocated to building bridges, public transit, airports, and railways. This level of investment can result in higher demand for Trimble’s civil engineering and construction software services for design and project management.

Another challenge faced in the construction industry is higher costs for materials.

As discussed above regarding the BCOM Index, the costs associated with procuring materials, though falling, still remains at elevated levels when compared to historical averages. Steel, being one of the commodities I most closely follow, has been on the rise in recent years given artificially suppressed supply. As I have referenced in previous articles, commodity producers have been heavily focused on producing to meet demand while maintaining market share. Cleveland Cliffs (CLF) has made it a point to not sell steel under their minimum required price, which was recently raised to $950/ton for hot rolled steel. This is the 6th time this year that Cleveland Cliffs has raised their minimum selling price, with a minimum price for HRC at $1,300/ton. US Steel (X), Nucor (NUE) and ArcelorMittal MT) have also set their minimums at higher rates, with Nucor at $900/ton for HRC and ArcelorMittal at $950/ton for HRC.

The question I’m raising is how this will affect future construction projects. Population migration and growth will continue to drive new builds in the multifamily and retail spaces, assuming office space demand remains stagnant, and single-family home construction will drive the need for more roads, power transmission, water, and other infrastructure. All of this should funnel into revenue growth for Trimble in the long run.

For a further analysis on Trimble, please follow the link to SeekingAlpha or subscribe to the paid subscription where I will discuss how to trade this company’s shares.

Keep reading with a 7-day free trial

Subscribe to ThePeachPit to keep reading this post and get 7 days of free access to the full post archives.